Concept project · 2025

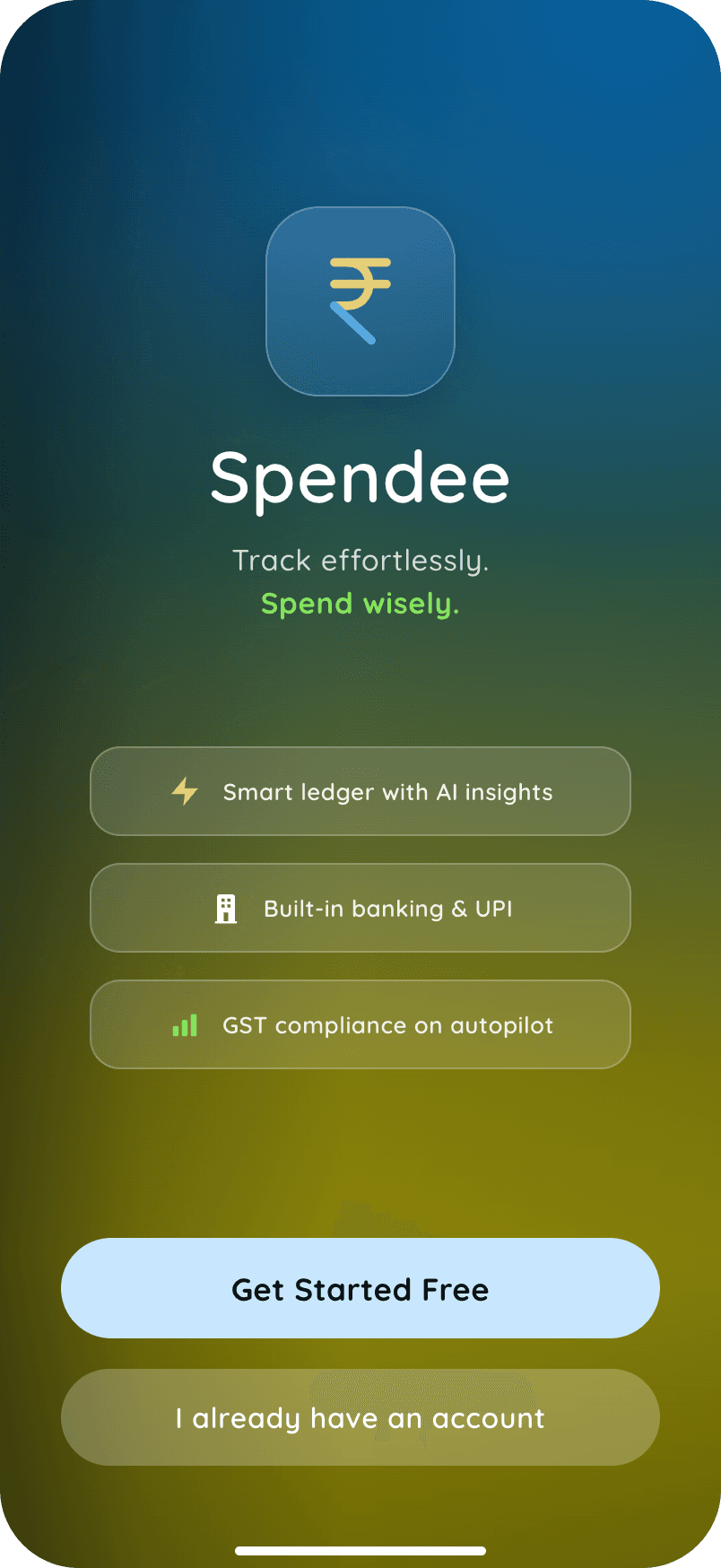

Spendee

A dark-mode finance super-app for Indian small businesses — ledger, GST, invoicing, payments, and credit in one legible interface.

- Role

- UI/UX & Product Design

- Year

- 2025

- Services

- UX Design, UI Design, Design System, Prototyping

Case study4 services · 19 screens

In one line

A ledger that earns its keep: GST mechanics, khata conventions, and cash-flow lending, compressed into an app one Kolkata trader could run — so good books become real working capital instead of paper a bank will never read.

Overview

Start with the object this app replaces: a paper khata — a bound ledger of who gave and who got, updated nightly, understood perfectly by its owner and legible to absolutely no one else. Spendee is a concept that takes everything orbiting that book — GST filing, invoicing, UPI collection, the loan application the bank keeps refusing — and folds it into one dark-mode app where the khata's own logic still runs the show. I owned the information architecture, the flows, the UI across every screen, and the design system that holds it together.

The domain

A small-business owner in India usually keeps their books in a paper khata or a basic ledger app, files GST through a separate portal or an accountant, raises invoices somewhere else, collects over UPI, and chases working capital from banks that never see their real cash position. India has over 63 million MSMEs, the overwhelming majority of them informal, and the day-to-day reality is one person stitching together half a dozen tools to run the money side of the business. Spendee lives in that world — the gap between how much these businesses transact and how little of that activity is captured, connected, and usable.

Problem

The data that proves a business is healthy never gets used to unlock the credit it qualifies for.

The information lives in silos, compliance deadlines sneak up, and a healthy business stays invisible to the lenders who could fund it. The owner loses time reconciling tools that don't talk to each other, GST obligations become a recurring source of stress, and the cash position that would qualify them for a loan is trapped in a paper ledger no bank will ever read.

The design challenge: bring all of it into one place, and make a dense, high-stakes, deadline-driven domain feel steady and in control rather than overwhelming.

Goals & signals

A first-time owner records their first ledger entry in under 30 seconds, without help.

Success signalTask completion without dead-ends in a short moderated test of the add-entry flow.

Untested hypothesisEvery screen leads with the next action, not just the numbers.

Success signalEach primary screen surfaces one unambiguous next step — 'File & Pay', 'Collect from 3 clients', 'Get ₹62k today'.

Design intentA stressful, easy-to-miss obligation — GST filing — feels like a guided task.

Success signalFrom the dashboard, an owner can see what's due and act in two taps or fewer.

Untested hypothesis

Research

No owners were interviewed for this concept. What's real here is the systems research: GSTR-1 and GSTR-3B filing mechanics, khata conventions, Account Aggregator and OCEN lending — read from the sources and from teardowns of the tools Indian SMBs actually use, not from users. Three things came out of that reading.

The workflow is genuinely fragmented across separate categories of product.

There's a mature tool for each job — Khatabook and OkCredit for the ledger, Vyapar and myBillBook for GST billing, the government GSTN portal (usually via an accountant) for filing, UPI apps for collection, and banks or NBFCs for credit — but no single dominant tool spans all of them. The "super-app" thesis isn't a hunch; it's a response to observable market segmentation.

The "I Gave / I Got" ledger entry is a convention, not an invention.

Every leading khata app models the core transaction as a binary gave-versus-got entry — the digital translation of the centuries-old paper bahi khata. Building on it is a deliberate decision to lower the learning curve, not a feature I dreamed up.

Good books unlocking credit mirrors a real shift in Indian lending.

The MSME credit gap is enormous and only a small fraction of these businesses can access formal credit, largely because they lack the financial records and collateral banks ask for. But underwriting is moving toward cash-flow and GST-data-based models — through the consent-driven Account Aggregator framework and OCEN — that assess repayment capacity from invoices and bank flows instead of paperwork. A ledger-health score built from on-time payments, inflow, and GST compliance is plausible precisely because that lending model already exists.

Strategy

A few decisions shaped the whole product.

Start from a model the owner already knows: "I Gave / I Got."

The core ledger entry is built on the khata mental model — money you gave (payable) versus money you got (receivable) — so the most frequent action feels familiar from the first use rather than like accounting software.

Colour is information, not decoration.

The entire app sits on near-black, which lets colour carry meaning: green for money in and settled, red for overdue and money out, amber for pending items and approaching deadlines. The eye learns the system once and reads every screen faster for it.

Surface the next action, not just the data.

Every screen leads with something to do — "File & Pay Now", "Collect from 3 clients", "Get ₹62k Today", "Apply in 2 Minutes" — turning passive numbers into prompts that move the business forward.

One consistent shell.

A five-slot bottom bar — Home, Ledger, a central add button, Bank, More — keeps the highest-frequency actions one tap away everywhere in the app, with a recurring header pattern (back · section label · title) so you always know where you are.

Design

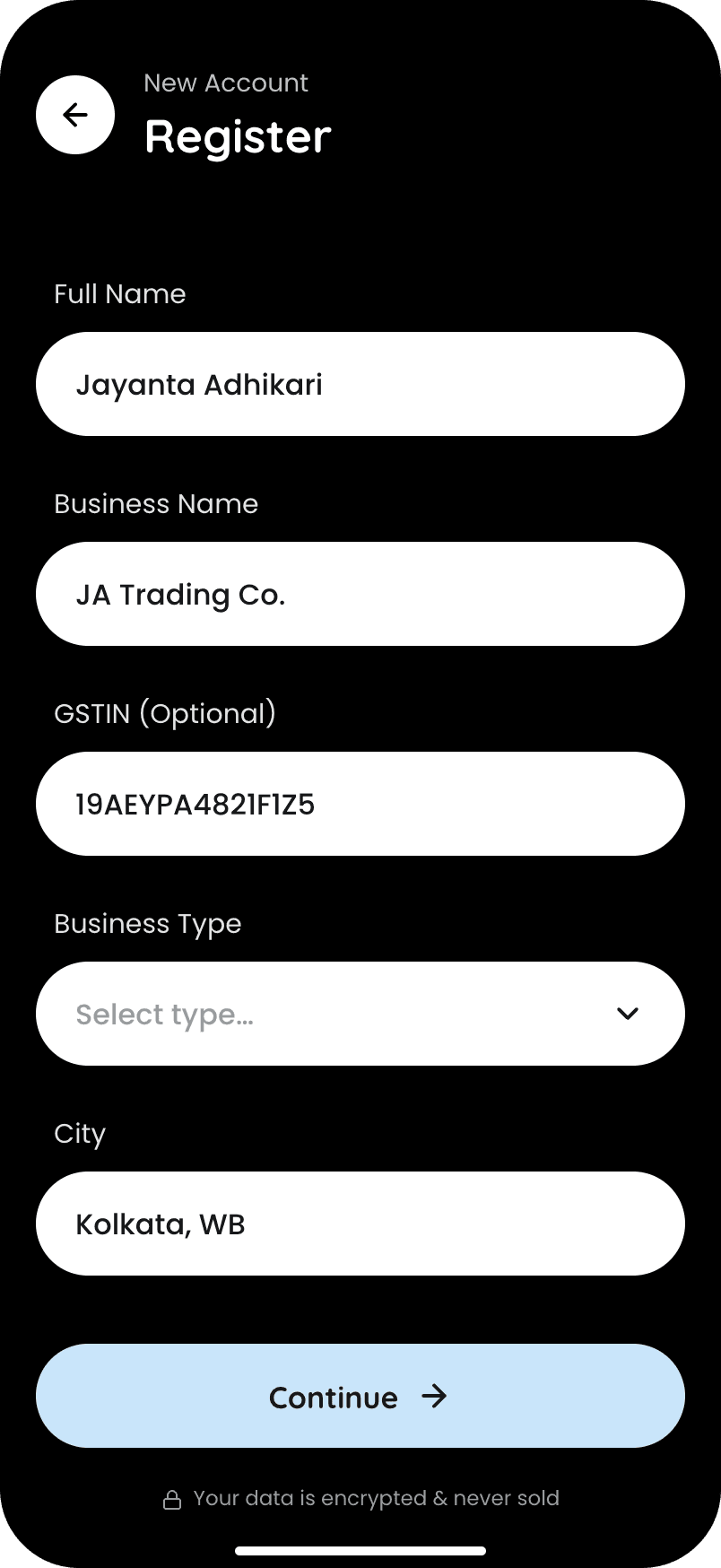

Onboarding & sign-in

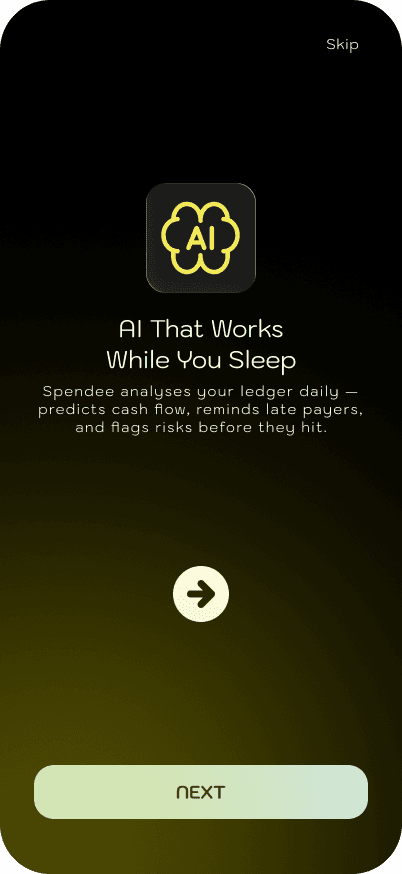

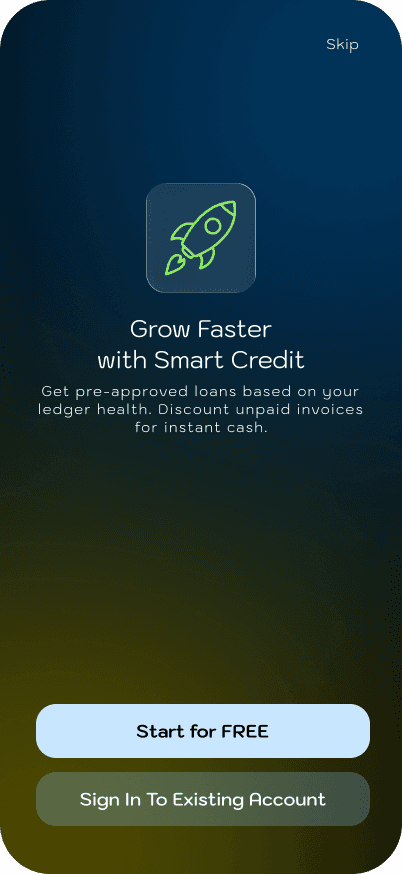

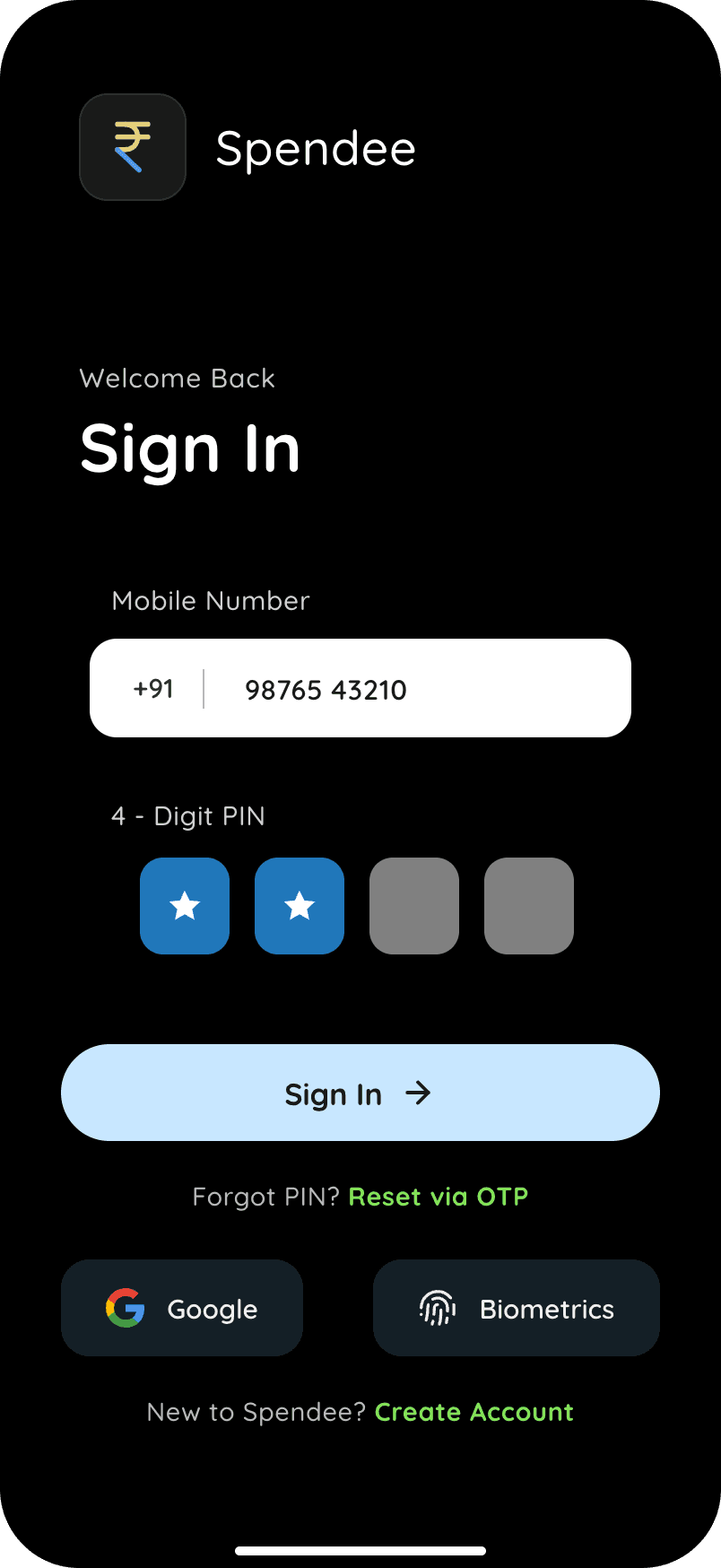

A short, four-step intro frames the value (a smart ledger, AI that watches your cash flow, credit built on your books) over a blue-to-lime gradient, before handing off to the quiet, near-black product. Auth is mobile-first: a four-digit PIN, biometrics, and Google, plus GSTIN capture at registration — built for how Indian small businesses actually onboard.

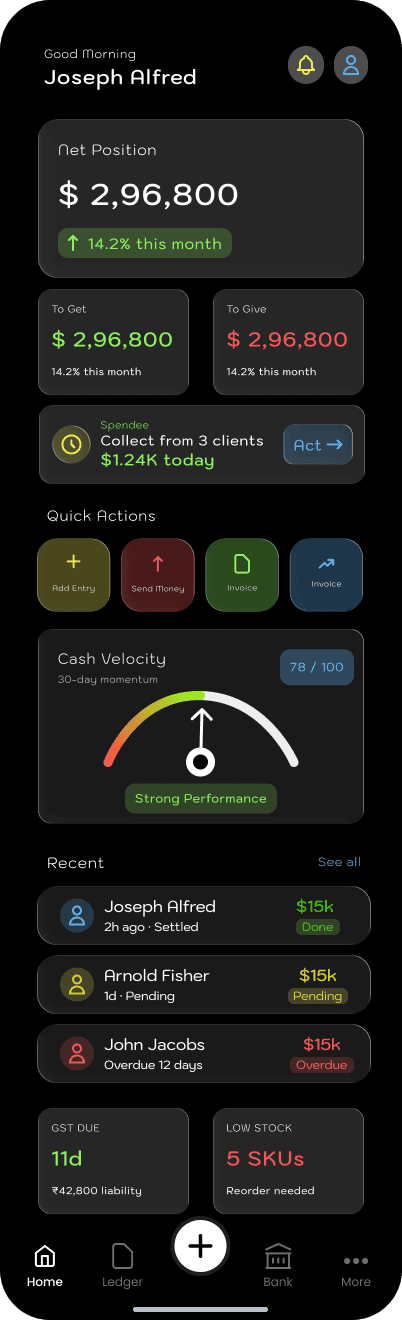

Dashboard

The home screen answers one question: how is my business right now? Net position with its monthly trend, money to get versus give, a cash-velocity gauge, quick actions, recent activity, and surfaced alerts for GST due and low stock — the whole state of the business above the fold.

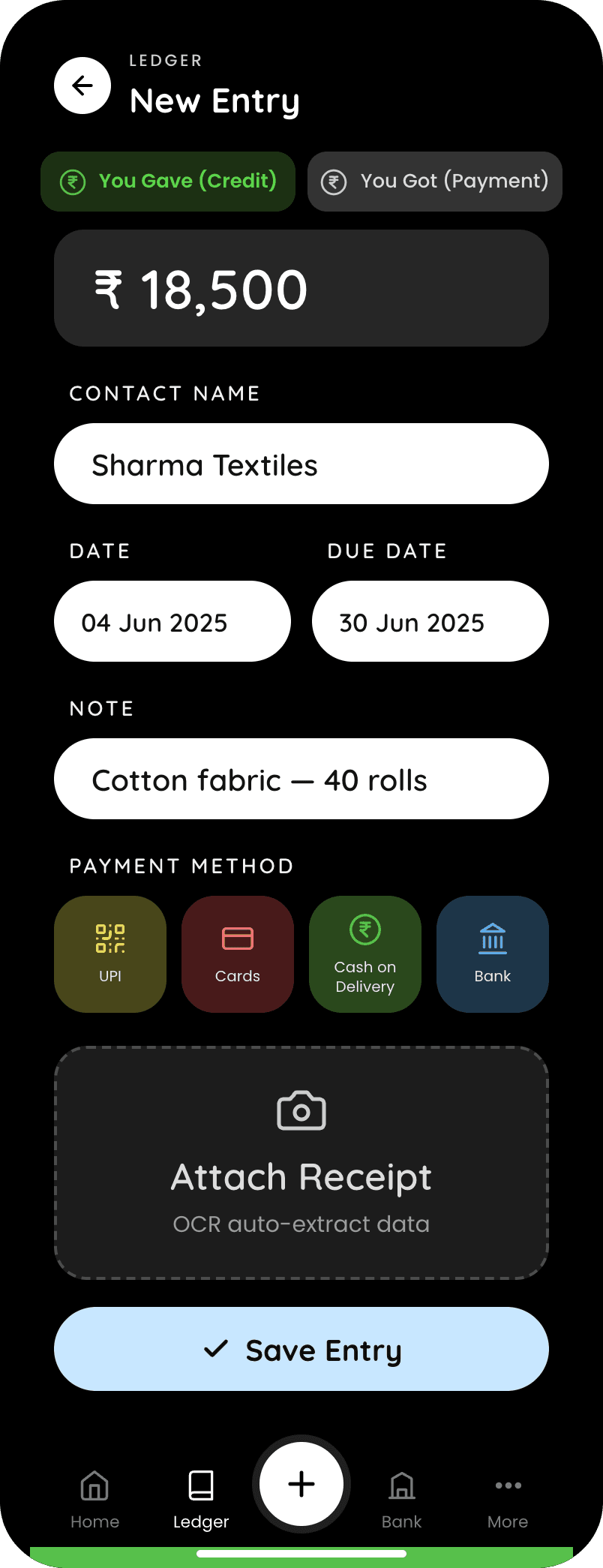

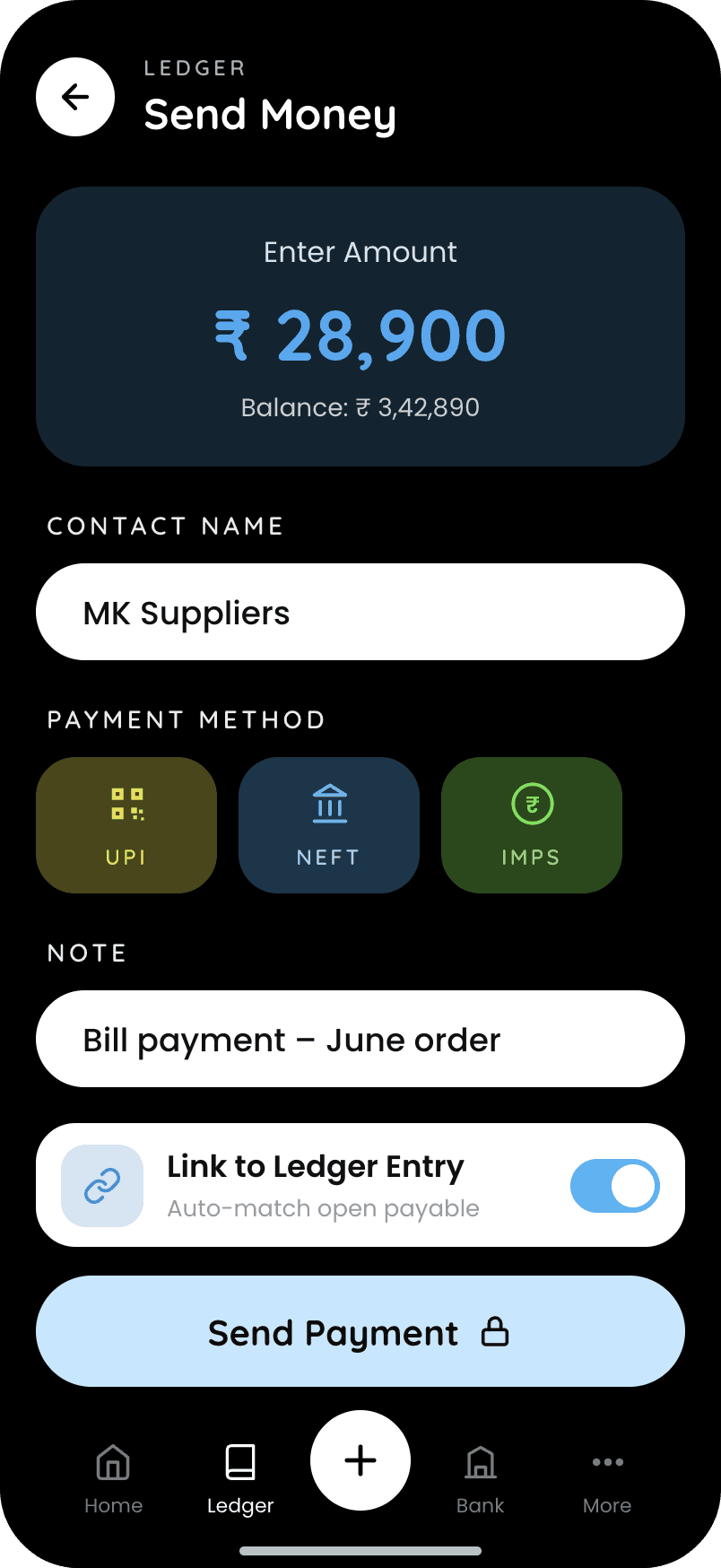

Ledger

Recording a transaction is the core loop: choose gave or got, enter the amount, contact, dates, and payment method, and attach a receipt that OCR reads automatically. Sending money links straight back to an open payable so the books stay reconciled.

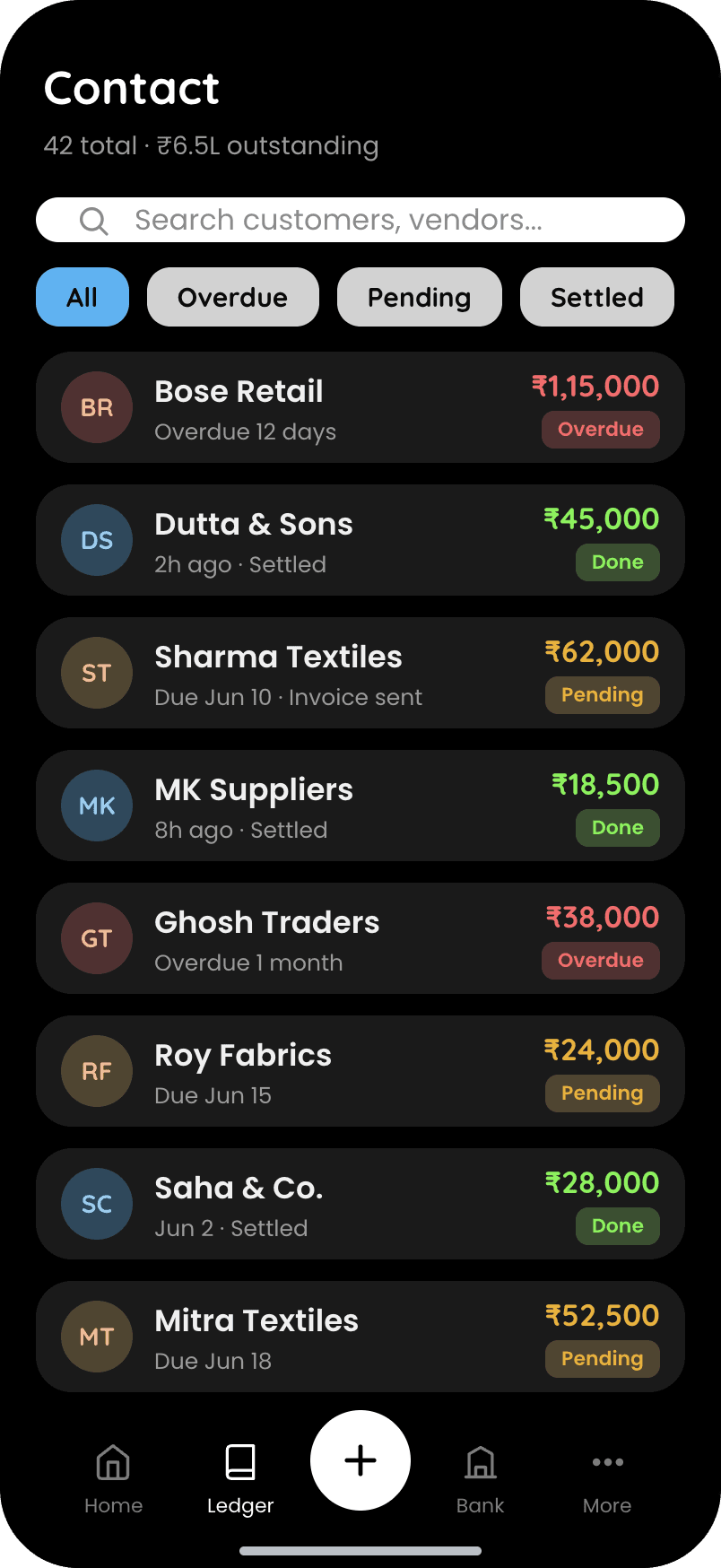

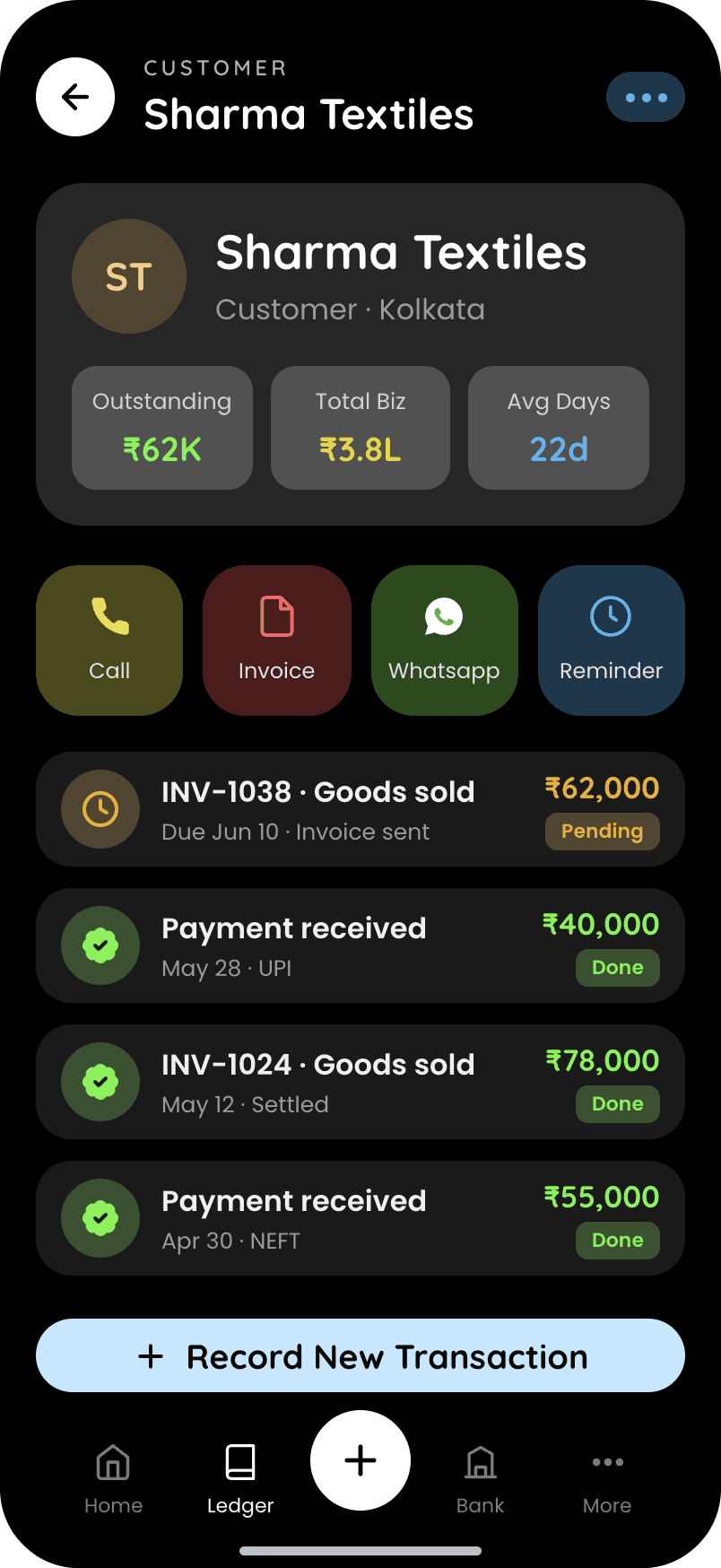

Contacts & invoicing

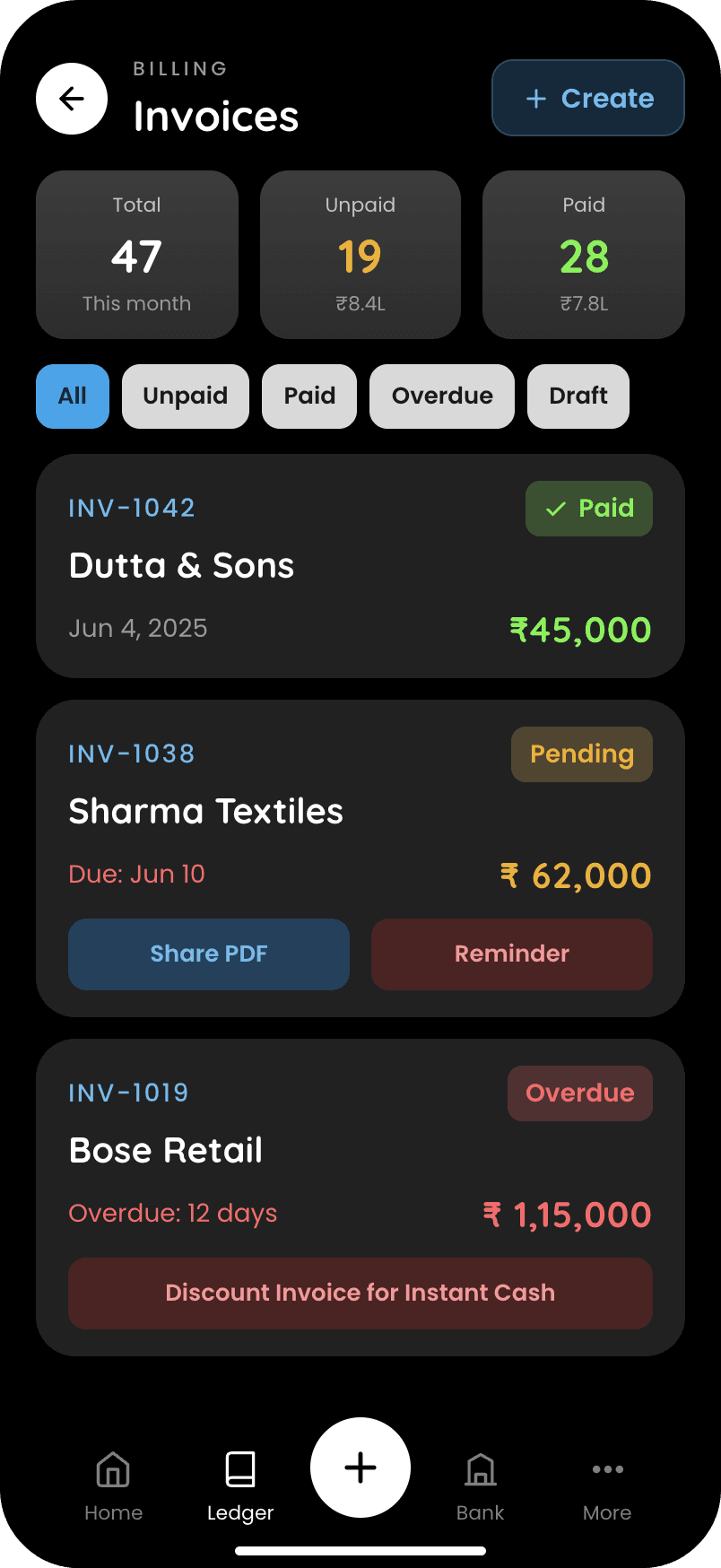

Every customer and vendor with their outstanding balance and status, filterable by overdue, pending, and settled, drilling into a per-contact history with one-tap call, invoice, WhatsApp, and reminders. Invoices get created, tracked, and chased by status, with share-as-PDF and reminders — and for overdue invoices, the option to discount them for instant cash.

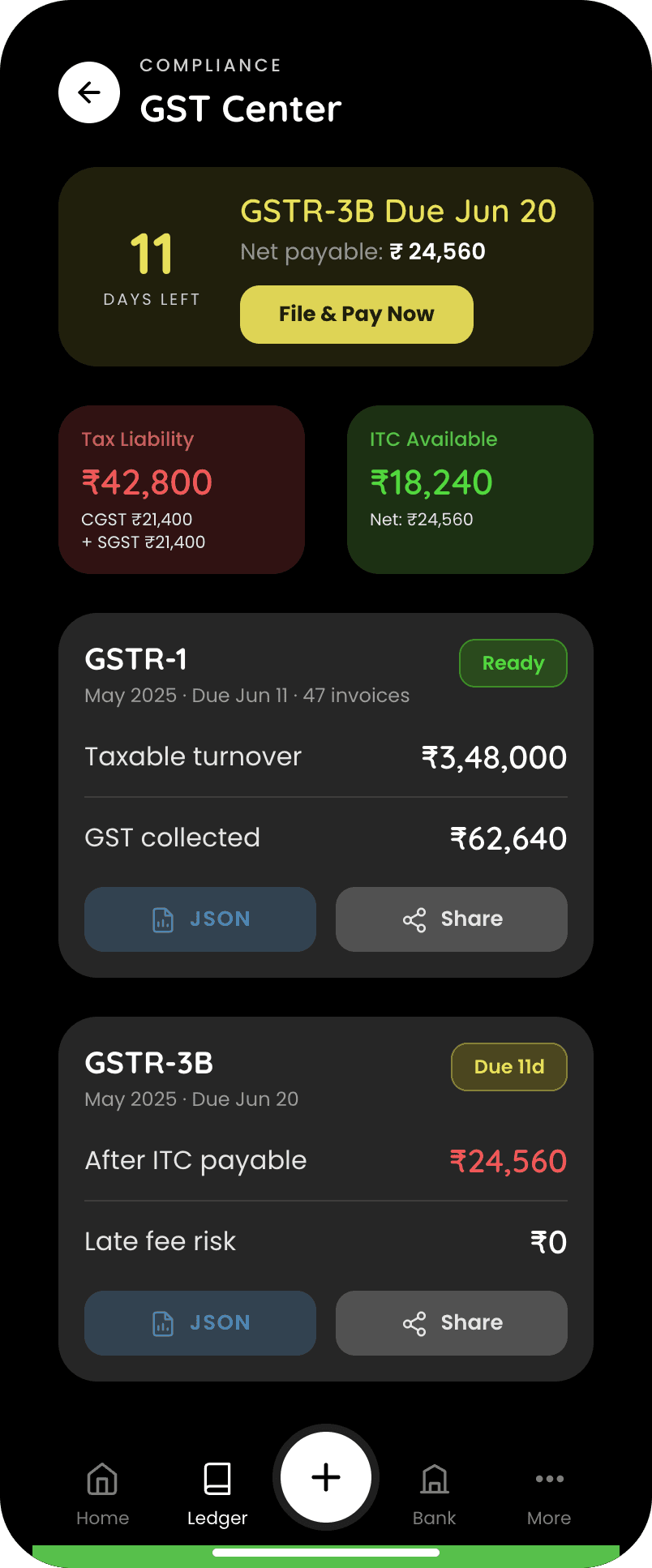

GST Center

The compliance hub, and the screen I'm most proud of: GSTR-3B and GSTR-1 summaries, tax liability against available input tax credit, deadline countdowns, and one-tap file-and-pay. GST filing carries real, recurring pressure — GSTR-1 by the 11th and GSTR-3B by the 20th, filed in sequence, with input-tax-credit reconciliation and per-day late fees on top. The GST Center turns that stressful, easy-to-miss obligation into a guided task.

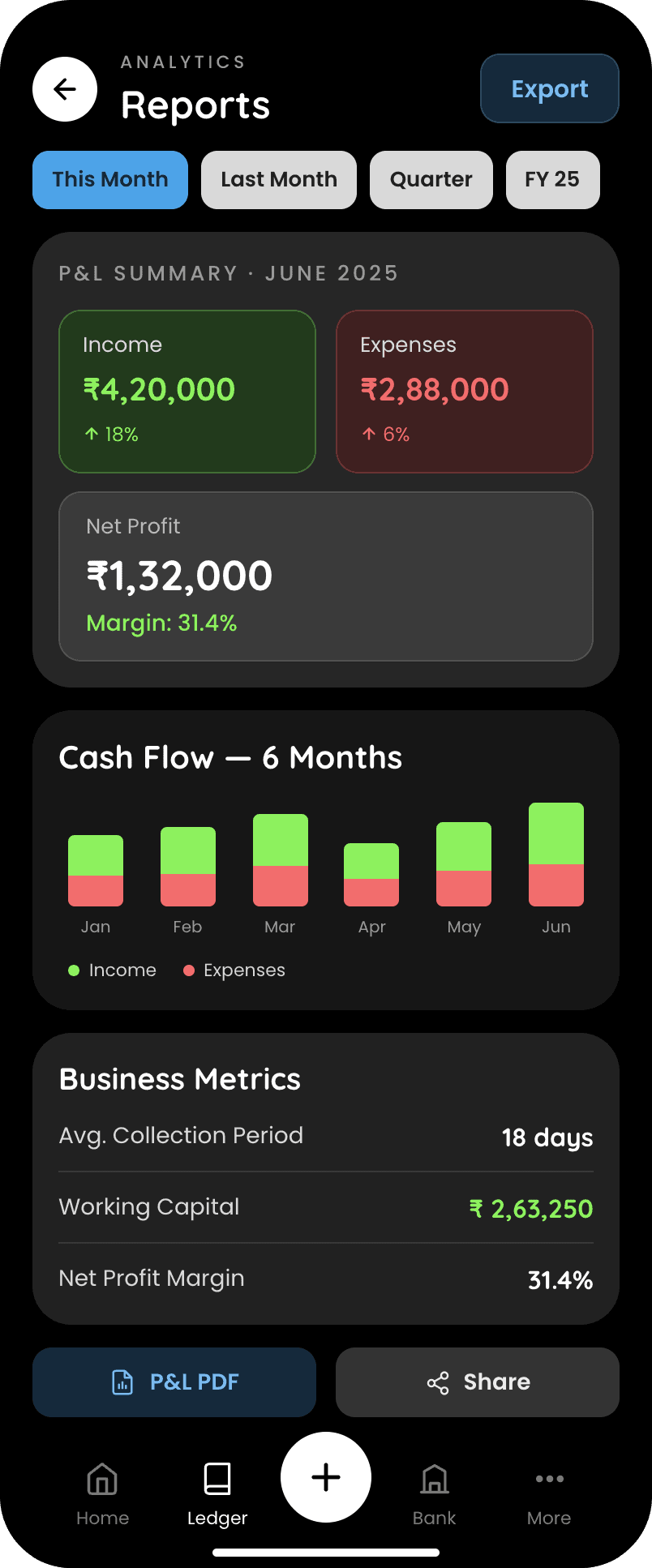

Reports

A P&L summary, a six-month cash-flow chart, and the metrics owners actually act on — average collection period, working capital, gross margin — exportable as a PDF.

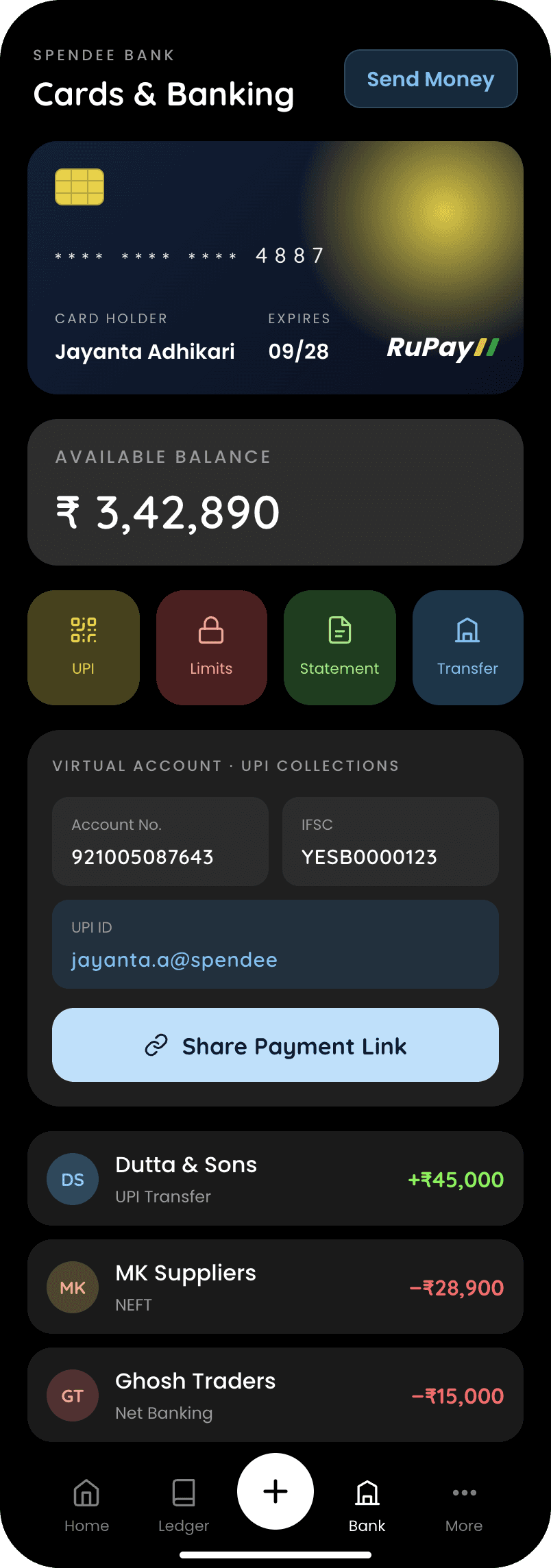

Banking

A built-in account with card, balance, a virtual account for UPI collections, and a shareable payment link, alongside transaction history. Designing collection around UPI reflects where Indian SMB payments actually are — overwhelmingly QR and UPI-first, driven by exactly these small and micro merchants.

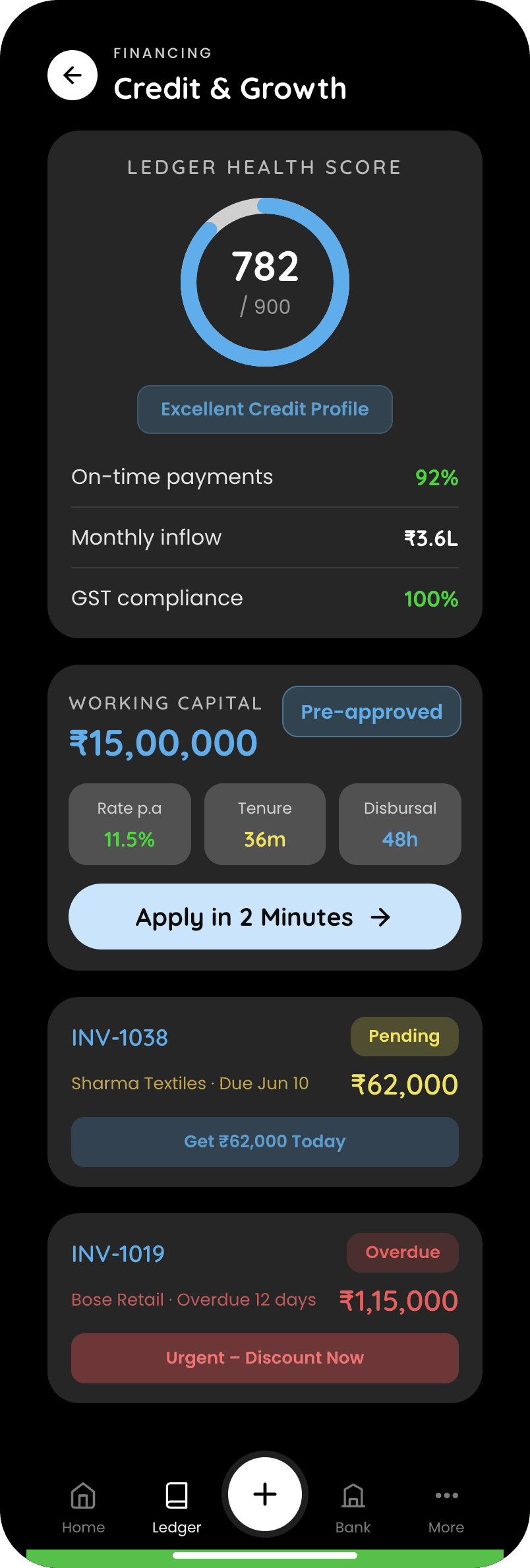

Credit & Growth

The payoff of keeping good books: a ledger-health score built from on-time payments, inflow, and GST compliance, used to pre-approve working capital and let owners discount specific invoices for cash. This is the thread that ties the whole product together — good data in the ledger becomes real financial leverage.

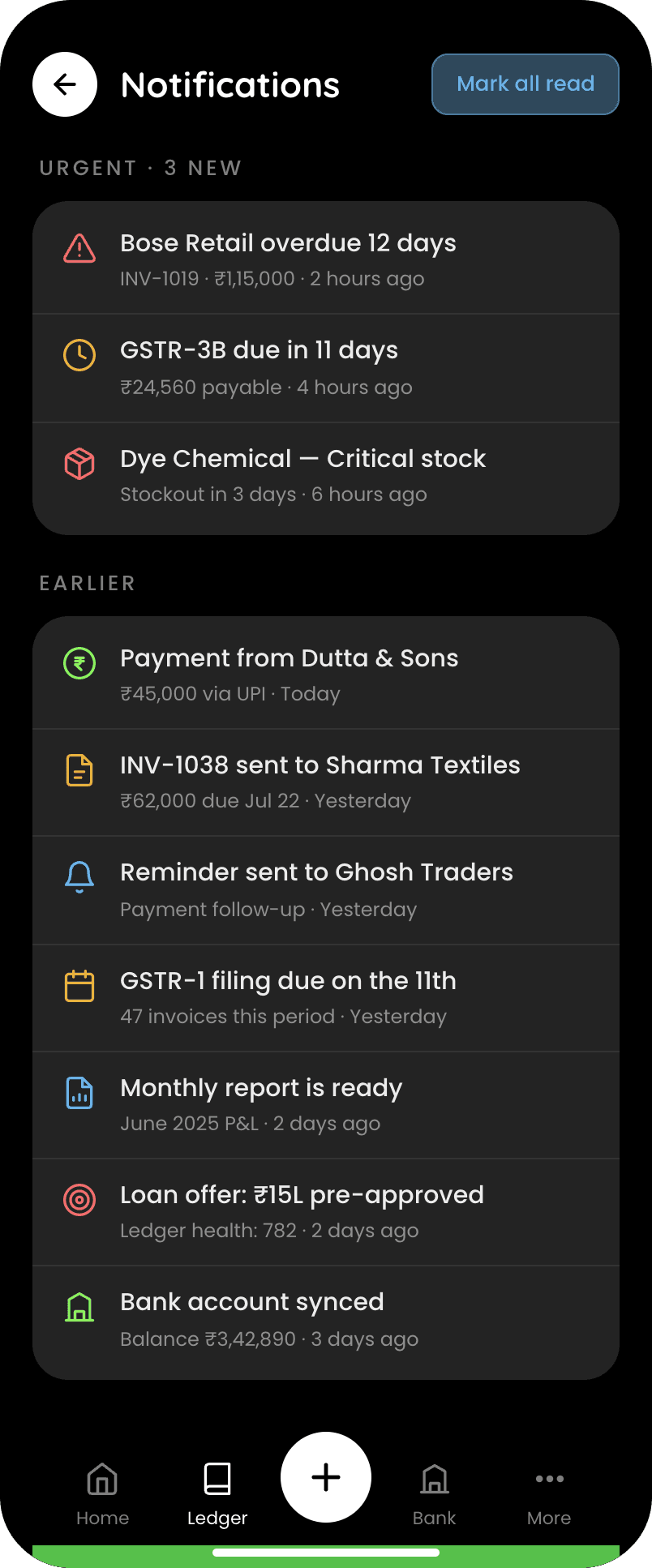

Notifications & settings

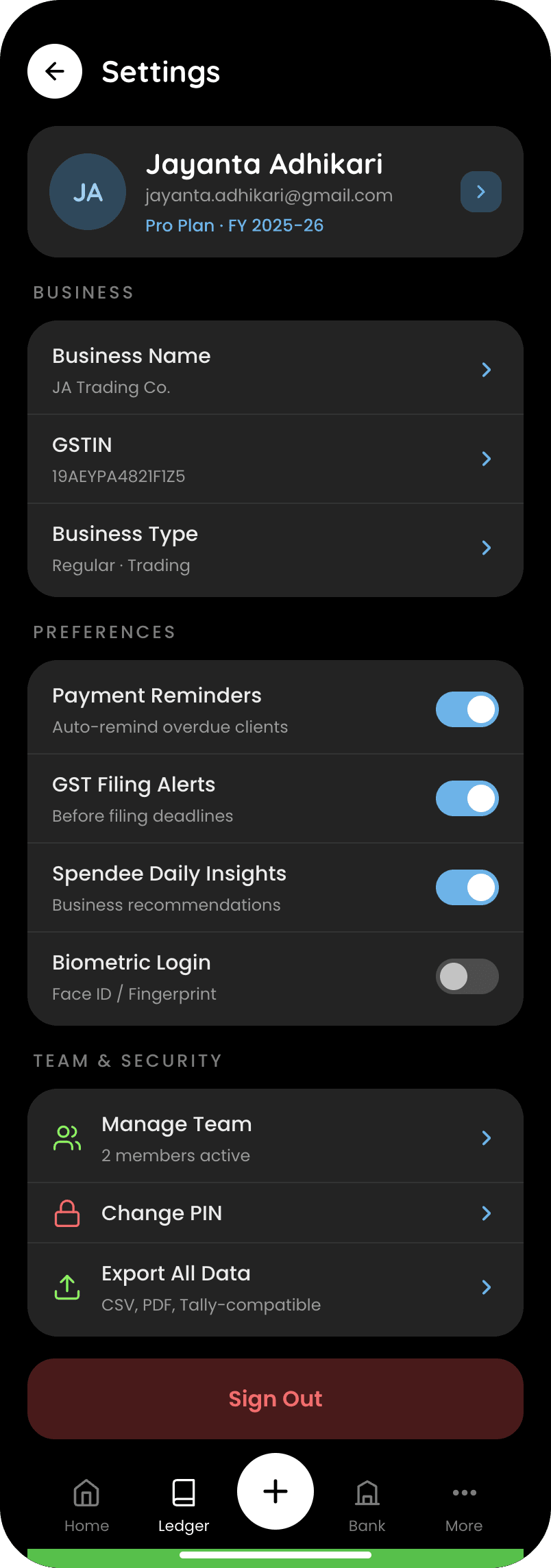

Prioritised alerts split into urgent and earlier — overdue payments, filing deadlines, low stock — plus a settings hub for business profile, reminders, team access, and Tally-compatible data export.

What revision caught

Concept work has no users to test with, so the only honest process evidence is revision — and this study needed it. The first pass of the dashboard priced a rupee-native ledger in dollars and shipped placeholder arithmetic: To Get, To Give, and Net Position all read the same ₹2,96,800, which no real ledger could produce, and two quick-action tiles were both labelled Invoice. The audit caught all of it; the shipped screen runs one coherent spine (₹4,15,200 − ₹1,18,400 = ₹2,96,800) that every other screen in the study reconciles against.

V1 — caught in revision

Shipped

Craft

One dark surface; a status colour system (green / red / amber) that encodes meaning across the app; rounded cards as the primary container; a consistent header pattern; the five-slot bottom navigation with a central add button; and a rounded, slightly geometric display face paired with a clean UI sans.

- Green — Settled / InMoney received, paid, reconciled

- Red — Overdue / OutPast due, money owed, action needed

- Amber — PendingAwaiting payment, approaching deadlines

Screens

A walk through the experience

19 screens · 6 flows01

Onboarding & sign-in

06 screensA four-step intro frames the value, then mobile-first auth with a PIN, biometrics, and GSTIN capture.

Welcome

Smart ledger

AI cash-flow

Credit on your books

Sign in

Sign up + GSTIN

02

Daily ledger

03 screensThe core loop — see the business at a glance, then record money you gave or got.

Dashboard

Add entry

Send money

03

Contacts & invoicing

03 screensEvery customer and vendor with their balance — call, invoice, and chase in a tap.

Contacts

Customer detail

Invoices

04

Compliance & reporting

02 screensGST filing turned into a guided task, plus the metrics owners actually act on.

GST Center

Reports

05

Banking & credit

02 screensA built-in account and a ledger-health score that turns good books into working capital.

Spendee Bank

Credit & Growth

06

Account

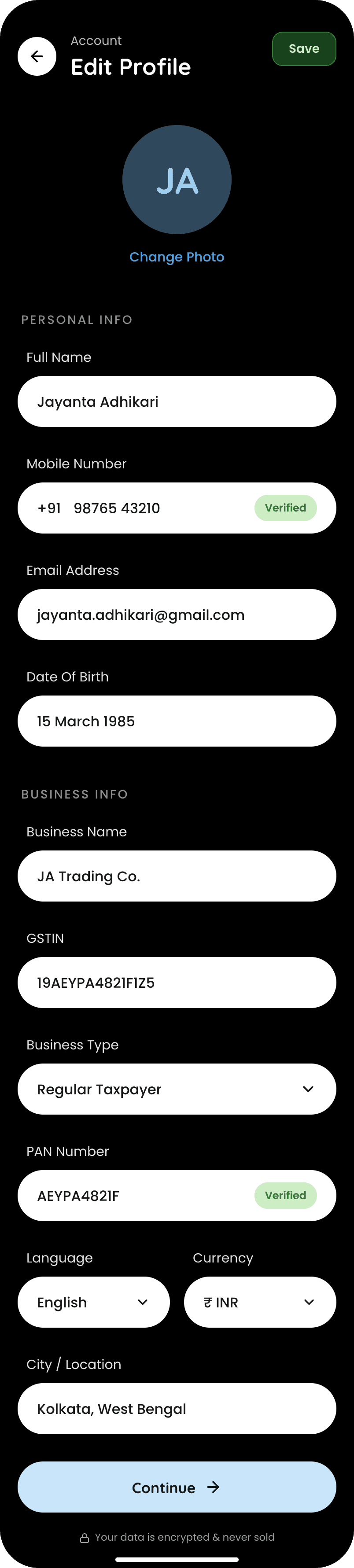

03 screensPrioritised alerts, a settings hub, and the business profile.

Notifications

Settings

Edit profile

Outcome

A concept has no launch metrics, so these are the constraints the design answers — the fixed points every screen had to respect.

- filing deadlines built around — the 11th and the 20th

- 2

- one tax spine, coherent across five screens

- ₹24,560

- ledger-health score, CIBIL-style, out of 900

- 782

- status colours carrying all the meaning

- 3

Reflection

The honest question for this product isn't whether the screens work — it's what would kill it. The khata-app category is crowded, cheap or free, and brutal to monetize; mature competitors have struggled toward profitability doing exactly the parity features Spendee also carries.

What I'd do next with real access: watch five owners record a day of entries against their paper khata and count where the app's model diverges from theirs, then pressure-test the GST Center against a real filing month — deadlines, credit reconciliation, late fees — with an accountant in the room.

Next departureVoyagerView case study